Limited Dependent Variables

EC655 - Econometrics

Justin Smith

Wilfrid Laurier University

Fall 2023

Introduction

Introduction

Many economic outcomes are qualitative in nature

Grouped into categories

Work or not

Drive, take bus, cycle to work

Number of visits to Doctor

People sometimes use alternative methods in this context

- Though linear regression does still work in many cases

In this section we cover models for these types of variables

Binary Choice Models

Linear Probability Model

Potential Outcomes

Start with the same potential outcomes setup

\(y_{1}\) is the outcome with treatment

\(y_{0}\) is the outcome without treatment

\(w\) is a binary variable with 1 denoting treatment, and 0 no treatment

We observe \((y, w)\), where

\[y = y_{0} + (y_{1} -y_{0})w\]

- Key difference here is that \(y_{1}\) and \(y_{0}\) are binary

\[y_{0} \in \{0,1\}\] \[y_{1} \in \{0,1\}\]

Linear Probability Model

Regression

- The slope in a regression of \(y\) on \(w\) is

\[E(y|w=1) - E(y|w=0)\] \[= \left [ E(y_{1}|w=1) - E(y_{0}|w=1) \right ] + E(y_{0}|w=1) - E(y_{0}|w=0)\]

First part is ATT, second part is selection bias

Mechanics are the same as when we had continuous outcomes

There is a difference in interpretation

\(y\) is a Bernoulli random variable,

\[E(y|w) = 1 \times Pr(y=1|w) + 0 \times Pr(y=0|w) = Pr(y=1|w)\]

Linear Probability Model

So you can restate the difference in observed means as

\[Pr(y=1|w=1) - Pr(y=1|w=0)\] \[= \left [ Pr(y_{1}=1|w=1) - Pr(y_{0}=1|w=1) \right ] + Pr(y_{0}=1|w=1) - Pr(y_{0}=1|w=0)\]

You can interpret as the difference in response probabilities

Difference in response probabilities is causal effect if

Independence of potential outcomes

Mean independence of potential outcomes

Conditional mean independence of potential outcomes

Linear Probability Model

What the above says is that regression still works when the treatment is binary

Causal effects depend on same assumptions as before

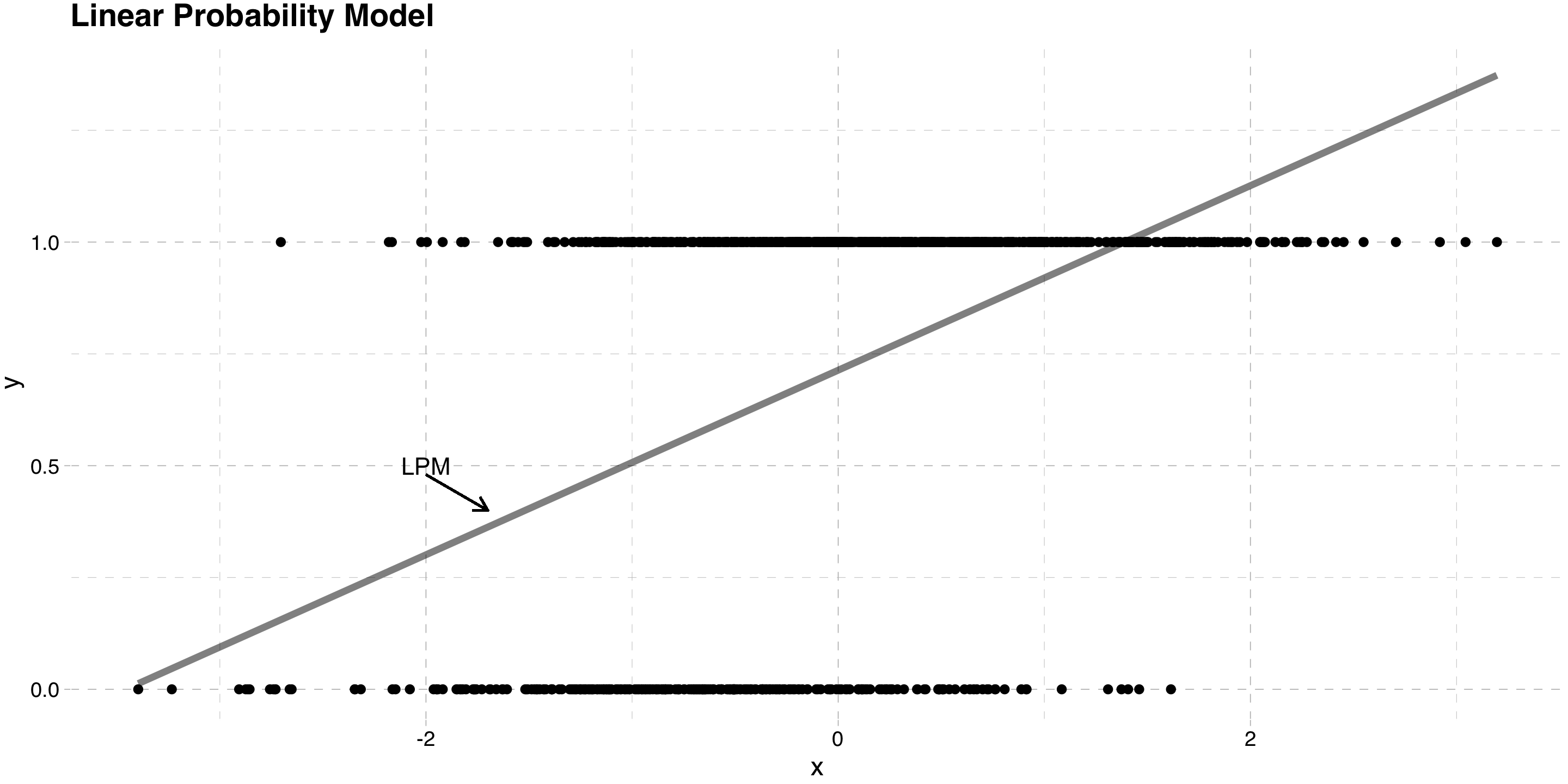

To estimate, use OLS regression of \(y\) on \(w\)

When \(y\) is binary, this is called the Linear Probability Model

Linear Probability Model

Issues with Linear Probability Model

Main problem is predicted probabilities can go outside [0,1] interval

- Some chance of nonesense probabilities

Mainly a problem of predictions

In most economic applications, we care about the slope

- So nonsense predictions are not a big problem

Linear Probability Model

The model exhibits heteroskedasticity

The population least squares regression of \(y\) on \(w\) is

\[y = \beta_{0} + w\beta_{1} + u\]

- The conditional variance of the error is

\[Var[u|w] = Var[y|w] = E[y^2|w] - E[y|w]^2\]

- Since \(y\) is binary, \(y^2 = y\), so

\[Var[y|w] = E[y|w] - E[y|w]^2\]

\[= E[y |w] (1-E[y|w])\]

Linear Probability Model

- Finally \(E[y|w] = Pr(y=1|w)\), so

\[Var[u|w] = Pr(y=1|w) (1-Pr(y=1|w))\]

This means that the variance of the error term is a function of \(w\)

It introduces heteroskedasticity into the model

Solution: use heteroskedasticity robust standard errors

Linear Probability Model

Nonlinear Models

Background

In some cases we may want to fix the predicted probability issue

- If you are doing prediction, for example

One way to do this is to feed the model through a CDF

This is often motivated with an index model

Suppose we model some latent variable \(y^*\) as

\[y^* = \beta_{0} + \beta_{1}w + e\]

- It is some underlying continuous outcome driving our decisions

Nonlinear Models

Issue is we do not observe \(y^*\)

Instead, we observe the binary \(y\) where

\[y = 1\{y^*>0\}\]

- Plugging the model into this

\[y = 1\{\beta_{0} + \beta_{1}w +e>0\}\]

- The probability that \(y=1\) is therefore

\[Pr(y=1|w) = Pr(\beta_{0} + \beta_{1}w +e>0 |w)\]

Nonlinear Models

- The random component is \(e\), so rearrange to isolate it

\[Pr(y=1|w) = Pr(e > -\beta_{0} - \beta_{1}w |w)\] \[ =1 - F(-\beta_{0} - \beta_{1}w)\] \[ =F(\beta_{0} + \beta_{1}w)\]

\(F()\) is the probability distribution of \(e\)

- \(1 - F(-\beta_{0} - \beta_{1}w) = F(\beta_{0} + \beta_{1}w)\) because \(F()\) is symmetric

The probability that \(y\) equals 1 depends on

Treatment status \(w\)

The distribution of \(e\)

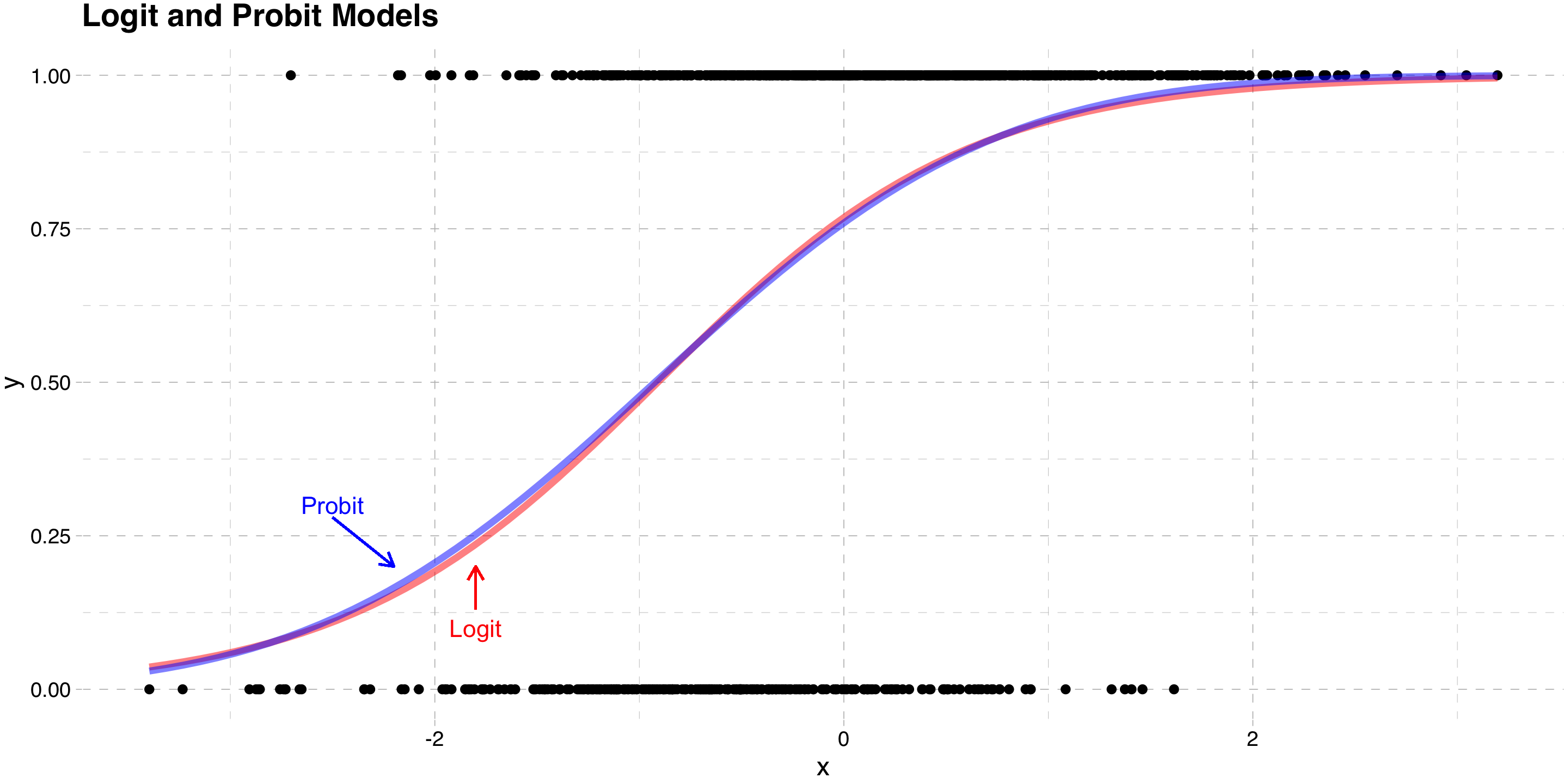

Different choices for \(F()\) distribution lead to different models

Nonlinear Models

Probit Model

- Assuming \(e \sim \mathcal{N}(0,\sigma^{2}_{e})\) leads to the Probit Model

\[Pr(y=1|w) = \Phi \left(\frac{\beta_{0} + \beta_{1}w}{\sigma^{2}_{e}} \right)\]

- where

\[\Phi (z) = \int_{-\infty}^{z} \frac{1}{\sqrt{2\pi}} e^{\frac{-v^2}{2}}\,dv\]

Because \(\Phi(.)\) is a CDF, \(Pr(y=1|w)\) is always between 0 and 1

- This solves the predicted probability problem

Nonlinear Models

- The difference in probabilities between treatment and control is

\[Pr(y=1|w = 1) - Pr(y=1|w=0)\] \[= \Phi \left(\frac{\beta_{0} + \beta_{1}}{\sigma^{2}_{e}} \right) - \Phi \left(\frac{\beta_{0}}{\sigma^{2}_{e}} \right)\]

Notice that \(\beta_{1}\) does not equal the difference in response probabilities

They are the slopes in the index model

The index model parameters are not usually of interest

To get the difference in response probabilities, feed parameters into the CDF first

In nonlinear models, parameters are not “marginal effects”

- You need to separately compute them after estimating the model

Nonlinear Models

- In models with more variables and where they are continuous

\[Pr(y=1|\mathbf{x}) = \Phi \left(\frac{\mathbf{x}\boldsymbol{\beta}}{\sigma^{2}_{e}} \right)\]

- The marginal effect for continuous variable \(x_{j}\)

\[\frac{\partial Pr(y=1|\mathbf{x})}{\partial x_{j}} = \phi \left(\frac{\mathbf{x}\boldsymbol{\beta}}{\sigma^{2}_{e}} \right) \frac{\beta_{j}}{\sigma^{2}_{e}}\]

This is a function of the entire vector \(\mathbf{x}\)

You need to specify their values to get the marginal effect

Normally people hold them at the mean

In theory you can get a distribution of marginal effects

Nonlinear Models

Logit Model

- Assuming \(e \sim \text{Logistic}(0,\sigma^{2}_{e})\) leads to the Logit Model

\[Pr(y=1|w) = \Lambda \left(\frac{\beta_{0} + \beta_{1}w}{\sigma^{2}_{e}} \right)\]

where

\[\Lambda (z) = \frac{e^z}{1+e^z}\]

Again, because \(\Lambda(.)\) is a CDF, \(Pr(y=1|w)\) is always between 0 and 1

Nonlinear Models

- The observed difference in probabilities is

\[Pr(y=1|w = 1) - Pr(y=1|w=0)\] \[= \Lambda \left(\frac{\beta_{0} + \beta_{1}}{\sigma^{2}_{e}} \right) - \Lambda \left(\frac{\beta_{0}}{\sigma^{2}_{e}} \right)\]

- In models with more variables and where they are continuous

\[Pr(y=1|\mathbf{x}) = \Lambda \left(\frac{\mathbf{x}\boldsymbol{\beta}}{\sigma^{2}_{e}} \right)\]

Nonlinear Models

- The marginal effect for continuous variable \(x_{j}\)

\[\frac{\partial Pr(y=1|\mathbf{x})}{\partial x_{j}} = \Lambda \left(\frac{\mathbf{x}\boldsymbol{\beta}}{\sigma^{2}_{e}} \right) \left( 1-\Lambda \left(\frac{\mathbf{x}\boldsymbol{\beta}}{\sigma^{2}_{e}} \right) \right)\frac{\beta_{j}}{\sigma^{2}_{e}}\]

- Again, this is a function of the full set of variables

Nonlinear Models

Estimation of Probit and Logit

Both models usually estimated by Maximum Likelihood

Method maximizes the probability of getting our sample by choosing parameters

- TheLikelihood Function is the function of the parameters given the data

The probability distribution of \(y_i\) is

\[f(y_i| \mathbf{x_{i}};\boldsymbol{\beta})= F \left(\frac{\mathbf{x_{i}}\boldsymbol{\beta}}{\sigma^{2}_{e}} \right)^{y_i} \left(1- F \left(\frac{\mathbf{x_{i}}\boldsymbol{\beta}}{\sigma^{2}_{e}} \right) \right) ^{1-y_{i}}\]

Nonlinear Models

- The joint probability of observing the all the \(y_{i}\) in the data is

\[f(\mathbf{y}| \mathbf{X};\boldsymbol{\beta})=\Pi_{i=1}^n F \left(\frac{\mathbf{x_{i}}\boldsymbol{\beta}}{\sigma^{2}_{e}} \right)^{y_{i}} \left(1- F \left(\frac{\mathbf{x_{i}}\boldsymbol{\beta}}{\sigma^{2}_{e}} \right) \right) ^{1-y_{i}}\]

- The Likelihood Function recasts as a function of the parameters given the data

\[\mathcal{L}(\boldsymbol{\beta}|\mathbf{y}, \mathbf{X})=\Pi_{i=1}^n F \left(\frac{\mathbf{x_{i}}\boldsymbol{\beta}}{\sigma^{2}_{e}} \right)^{y_{i}} \left(1- F \left(\frac{\mathbf{x_{i}}\boldsymbol{\beta}}{\sigma^{2}_{e}} \right) \right) ^{1-y_{i}}\]

Nonlinear Models

Both models usually estimated by Maximum Likelihood

Method maximizes the joint probability of \(y\) values conditional on \(\mathbf{x}\)

- This is called the Likelihood Function

In the case of a binary \(y\), the likelihood function is

\[f[y| \mathbf{x};\boldsymbol{\beta}]=P[Y_{1} = y_{1}, Y_{2} = y_{2}, \ldots, Y_{n} = y_{n}|\mathbf{x_{i}};\boldsymbol{\beta}]\] \[=\Pi_{y_{i}=1}F \left(\frac{\mathbf{x_{i}}\boldsymbol{\beta}}{\sigma^{2}_{e}} \right) \Pi_{y_{i}=0} \left[1-F \left(\frac{\mathbf{x_{i}}\boldsymbol{\beta}}{\sigma^{2}_{e}} \right) \right]\] \[=\Pi_{i=1}^{n} F \left(\frac{\mathbf{x_{i}}\boldsymbol{\beta}}{\sigma^{2}_{e}} \right)^{y_{i}} \left[1-F \left(\frac{\mathbf{x_{i}}\boldsymbol{\beta}}{\sigma^{2}_{e}} \right)\right] ^{1-y_{i}}\]

Nonlinear Models

Researchers usually focus on the log of the likelihood instead

It is a monotonic (increasing) transformation of the likelihood

The same parameter vector solves both versions

Log likelihoods are easier to work with

Log Likelihood \[ln\mathcal{L}(\boldsymbol{\beta}|\mathbf{y}, \mathbf{X})= \sum_{i=1}^{N}\{ y_{i}lnF \left(\frac{\mathbf{x_{i}}\boldsymbol{\beta}}{\sigma^{2}_{e}} \right)+ (1-y_{i})ln (1-F \left(\frac{\mathbf{x_{i}}\boldsymbol{\beta}}{\sigma^{2}_{e}} \right)) \}\]

To solve this equation, you need numerical methods

- A grid search algorithm that finds the maximum value

Nonlinear Models

In ML environments, the estimated variance of \(\boldsymbol{\hat{\beta}}\) is estimated as the negative of the expected value of the Hessian (information matrix) \[\hat{Var}(\boldsymbol{\hat{\beta}}) = -E[(\frac{\partial^2 lnL}{\partial\boldsymbol{\hat{\beta}} \partial \boldsymbol{\hat{\beta}^{'}}})^{-1}]\] \[= (\sum_{i=1}^{n} \frac{f(\mathbf{x_{i}^{'}}\boldsymbol{\hat{\beta}})^2 }{ F(\mathbf{x_{i}^{'}}\boldsymbol{\hat{\beta}})(1- F(\mathbf{x_{i}^{'}}\boldsymbol{\hat{\beta}}) ) } \mathbf{x_{i}x_{i}^{'}} )^{-1}\]

where \(F(.)\) is either the Normal or Logistic CDF, and \(f(.)\) is the associated PDF

Nonlinear Models

Nonlinear Models

Hypothesis Testing in Probit and Logit

Simple tests for coefficient significance is done by the usual \(t\)-test method

Assume \(\boldsymbol{\hat{\beta}}\) has normal distribution (asymptotically)

Test statistic \(Z = \frac{\hat{\beta}_{k}}{\hat{SE}(\hat{\beta}_{k})}\)

Nonlinear Models

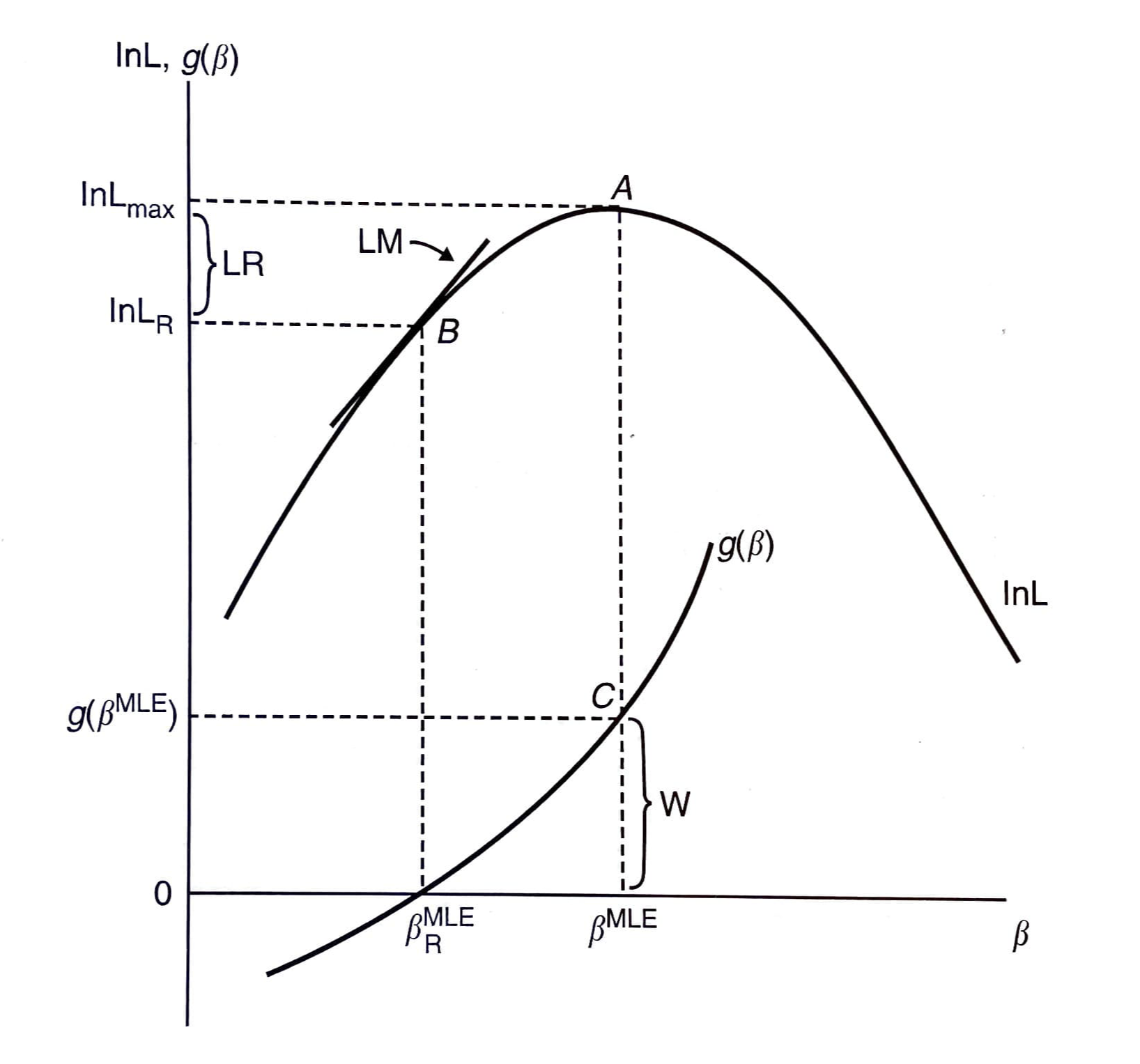

More complicated tests done using one of 3 methods:

Likelihood Ratio (LR) Test

Test statistic \(LR = 2[ln\hat{L}_{U} - ln\hat{L}_{R}]\)

\(ln\hat{L}_{R}\) is log likelihood evaluated at restricted parameter vector

Wald (W) Test

Test statistic \(W = \hat{g}^{'}[\hat{G}\hat{Var}(\boldsymbol{\hat{\beta}})\hat{G}^{'}]\hat{g}\)

\(\hat{g}\) is a vector of restrictions evaluated at \(\boldsymbol{\hat{\beta}}\)

\(\hat{G}\) is the derivative of a vector of restrictions evaluated at \(\boldsymbol{\hat{\beta}}\)

Lagrange Multiplier (LM) Test

Test statistic \(LM = \hat{d}^{'}[\hat{Var}(\boldsymbol{\hat{\beta}})]\hat{d}\)

\(\hat{d}\) is the derivative of \(lnL\) evaluated at restricted \(\boldsymbol{\hat{\beta}}\)

Restrictions can be linear or non-linear

Nonlinear Models

Nonlinear Models

Goodness of Fit in Probit and Logit

Confusion Matrix

Actual Predicted 0 1 Total 0 # Correct 0 # Incorrect 1 # Pred 0 1 # Incorrect 0 #Correct 1 # Pred 1 Total # True 0 # True 1 Pseudo-\(R^{2}\)

McFadden \(\rightarrow\) \(R^{2} = 1 - \frac{ln\hat{L}_{U}}{ln\hat{L}_{0}}\)

- \(ln\hat{L}_{0}\) is log-likelihood with no explanatory variables

Others are possible, but goodness of fit is not incredibly important

Limited Dependent Variables

Introduction

Arises when a continuous dependent variable is limited in its range

Censoring

- Income is top-coded at some level for privacy

Corner Solutions

- Spending on consumer durables limited below by 0

Incidental Truncation

- Wage is not observed for people who do not work

You can sometimes use OLS depending on context

We will cover models for censoring and corner solutions

Tobit Model

Latent Variable

- We again appeal to a latent variable model

\[y^{*} = \beta_{0} + \beta_{1}w + e\]

- Suppose the observed \(y\) is

\[y = max \{ 0,y^* \}\]

This would be the case for things like consumer purchases

You spend zero or some positive amount

It is naturally bounded below by zero

Tobit Model

- Because it is either zero or positive, the expected value of \(y\) is

\[E[y|w] = E[y|y>0,w]Pr[y>0|w]\]

- Taking the difference in the observed \(y\), we get

\[E[y|w = 1] - E[y|w = 0]\] \[= E[y|y>0,w=1]Pr[y>0|w=1] - E[y|y>0,w=0]Pr[y>0|w=0]\] \[=(Pr[y>0|w=1]-Pr[y>0|w=1]) E[y|y>0,w = 1]\] \[+ (E[y|y>0,w = 1] - E[y|y>0,w = 0]) Pr[y>0|w=0]\]

Tobit Model

There are two key pieces

Participation effect

Conditional on Positive effect

In terms of potential outcomes

\[E[y|w = 1] - E[y|w = 0]\] \[= E[y_1|w = 1] - E[y_0|w = 0]\] \[= E[y_1|w = 1] - E[y_0|w = 1] + E[y_0|w = 1] - E[y_0|w = 0]\]

The limited dependent variable does not change causal interpretation

- As long as potential outcome \(y_{0}\) is mean independent of treatment

Tobit Model

Conditional on Positive

In some contexts people run regressions with just the positive outcomes

- If you wanted to analyze participation decision separately

Difference in observed \(y\) for this group is biased if under random assignment

\[E[y|y>0,w = 1] - E[y|y>0, w = 0]\] \[= E[y_1|y_1>0] - E[y_0|y_0>0]\] \[= E[y_1|y_1>0] - E[y_0|y_1>0] + E[y_0|y_1>0] -E[y_0|y_0>0]\]

The treatment changes who has positive values of potential outcomes

- More subtle form of bias

You cannot interpret conditional on positive effects as causal

Tobit Model

Model

This model is used in the context of censoring and corner solutions

We have data on a random sample

The outcome is limited in its range

There is a mass of observations at 1 or more values

Usually zeroes

Sometimes some upper amount, like income

Using OLS may be a bad strategy depending on your goals

- Can produce predicted values outside the limited range

Tobit Model

- The Tobit model starts with the latent variable model

\[y^{*} = \mathbf{x}\boldsymbol{\beta} + e, \text{ where } e \sim N(0,\sigma^2_{e})\] \[y = \text{max}(0,y^{*})\]

The conditional expectation of interest depends on context

Censored data

\(E[y^{*}|\mathbf{x}]\)

\(y^{*}\) usually has meaning when data are censored

Corner Solutions

\(E[y|\mathbf{x}]\) and \(E[y|y>0, \mathbf{x}]\)

\(y_{i}^{*}\) usually has no meaning for corner solutions

This is the most common situation

Tobit Model

Estimation

Estimate this model by maximum likelihood

The likelihood function has two pieces

When \(y_{i} = 0\)

\[Pr(y_{i} = 0| \mathbf{x}) = Pr(y_{i}^{*}<0 |\mathbf{x})\] \[= Pr(\mathbf{x}\boldsymbol{\beta} +e<0 |\mathbf{x})\]

Tobit Model

- Due to symmetry in the distribution of \(e\)

\[= Pr(e>\mathbf{x}\boldsymbol{\beta} |\mathbf{x})\] \[= Pr(\frac{e}{\sigma_{e}}>\frac{\mathbf{x}\boldsymbol{\beta}}{\sigma_{e}} |\mathbf{x})\]

\[= 1-\Phi\left ( \frac{\mathbf{x}\boldsymbol{\beta}}{\sigma_{e}} \right)\]

Tobit Model

- When \(y_{i} > 0\)

\[f(y_{i} | y_{i}>0, \mathbf{x}) = \frac{1}{\sigma_{e}} \phi \left ( \frac{ y_{i} - \mathbf{x}\boldsymbol{\beta}}{\sigma_{e}} \right )\]

- Combining terms, we can form the likelihood function

\[\mathcal{L}(\boldsymbol{\beta}|\mathbf{y}, \mathbf{X}) =\Pi_{y_{i}=0} \left(1-\Phi\left ( \frac{\mathbf{x}\boldsymbol{\beta}}{\sigma_{e}} \right) \right ) \Pi_{y_{i}>0} \left( \frac{1}{\sigma_{e}} \phi \left ( \frac{ y_{i} - \mathbf{x}\boldsymbol{\beta}}{\sigma_{e}} \right ) \right)\]

Tobit Model

- The log likelihood is

\[ln\mathcal{L}(\boldsymbol{\beta}|\mathbf{y}, \mathbf{X}) =\sum_{y_{i}=0} ln \left(1-\Phi\left ( \frac{\mathbf{x}\boldsymbol{\beta}}{\sigma_{e}} \right) \right ) + \sum_{y_{i}>0} ln\left( \frac{1}{\sigma_{e}} \phi \left ( \frac{ y_{i} - \mathbf{x}\boldsymbol{\beta}}{\sigma_{e}} \right ) \right)\]

- Maximize this function by choosing the parameter vector \(\boldsymbol{\beta}\) and \(\sigma_{e}\)

Tobit Model

Marginal effects will depend on the context of our estimation

Censored data \[\frac{\partial E[y^{*}|\mathbf{x}]}{\partial x_{k}} = \beta_{k}\]

- In a Tobit with censored data, you can interpret the slope directly

Corner Solutions

\(\frac{\partial E[y|\mathbf{x}]}{\partial x_{k}} = \Phi(\frac{ \mathbf{x}\boldsymbol{\beta} }{\sigma})\beta_{k}\)

\(\frac{\partial E[y| y>0,\mathbf{x}]}{\partial x_{k}} = \{1-\lambda(\frac{ \mathbf{x}\boldsymbol{\beta} }{\sigma})[\frac{ \mathbf{x}\boldsymbol{\beta} }{\sigma} + \lambda(\frac{ \mathbf{x}\boldsymbol{\beta} }{\sigma})] \}\beta_{k}\)

With corner solutions it depends on what you want

You may want slope for random person, or conditional on \(y>0\)

Tobit Model

Issues with Tobit Model

It must be possible for the dependent variable to take values near the limit

Example: not the case with consumer durables

You either spend zero or a large amount

Intensive and Extensive margins have same parameters

Means the model is relatively inflexible

Can be solved by modelling each separately

Normality assumption

Care must be taken in interpreting the coefficients

- Do we care about the effect of \(x_{k}\) on \(y\) or \(y^{*}\)?